Stay updated with complimentary news alerts

Sign up for the Global Economy myFT Digest and receive updates directly to your email.

The phenomenon of “Japanification” in China remains a significant topic, with several striking similarities, especially in terms of stimulus effectiveness falling short. One recent development highlights this connection:

Currently, the 30-year government bond yields of China and Japan are approaching convergence for the first time (at least in available data since 2009).

As of now, there is a slight 8.7 basis point difference between the two long-term bond yields, with China’s 30-year yield at 2.245 and Japan’s at 2.158 per cent. However, this gap is expected to narrow in the near future. Shorting Chinese government bonds has become a challenging trade.

The diminishing yield curve disparity underscores China’s economic and demographic challenges, contrasted with Japan’s relative success in combating deflation over the past thirty years. In a comprehensive analysis on China’s potential trajectory, Barclays economists stated:

China’s rapid economic progress once mirrored Japan’s post-war economic boom. Initially forecasted to surpass the US as the world’s largest economy by 2035, China has now started to lag behind since 2022. The weakening labor market, declining corporate profitability, sluggish housing sector, and concerning debt-deflation dynamics have raised doubts about China’s future growth prospects.

. . . Our view is that China’s deleveraging process is still in its early stages and unlikely to conclude before 2030, implying persistent structural obstacles to consumption and investment.

Although there remains a noticeable albeit diminishing gap between China and Japan in the 10-year segment of the curve, yields have already intersected in the longer end. For instance, Japan’s government bond maturing in March 2064 currently yields 2.472 per cent, while China’s November 2064 bond trades at 2.275 per cent.

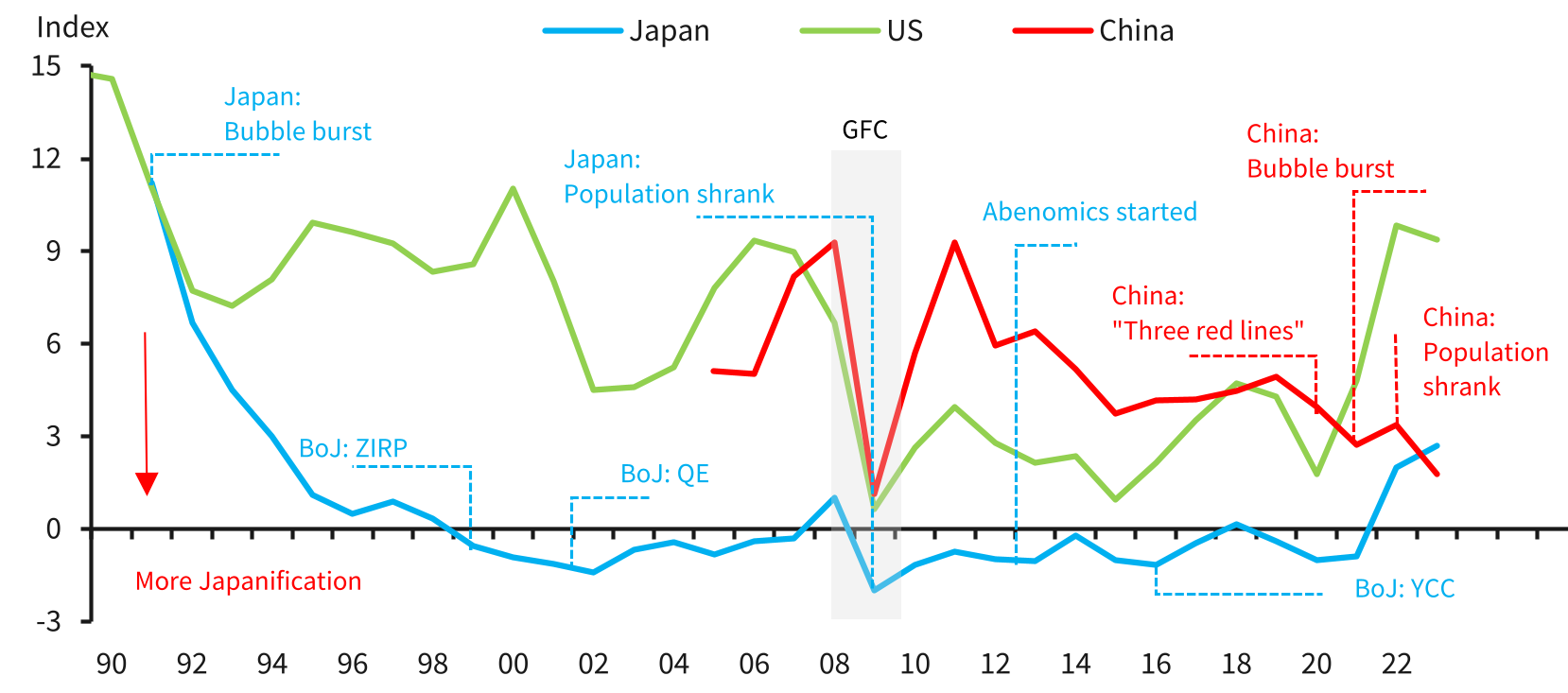

Barclays’ report draws attention to the numerous parallels between Japan in the early 1990s and China’s current situation. Particularly noteworthy is the impact of “Japanification” on both economies. Here is an excerpt from FT Alphaville’s coverage:

China’s economic challenges mirror Japan’s post-asset bubble burst experience in the early 1990s. This scenario, known as ‘Japanification,’ is characterized by slow growth, low inflation, a subdued policy rate, and unfavorable demographic trends.

To gauge this trend, Japanese economist Takatoshi Ito devised a Japanification Index, which combines the inflation rate, nominal policy rate, and GDP gap. To assess China’s situation, we have modified this index, replacing the GDP gap with working-age population growth, given variations in GDP gap estimation methods across countries. Our revised index reveals that China’s economy has become more ‘Japanised’ than Japan’s in recent times, albeit marginally.

This alignment is not surprising. Demographic challenges, cyclical asset bubble cycles, high debt levels, presence of zombie enterprises, deflationary pressures from surplus capacity/debt burdens, and elevated youth unemployment are among the shared characteristics of China and Japan post their respective bubbles.

Here is the link to the index discussed in the analysis.

{kind=link}