Important Highlights

- Economists are confident that the housing market is not heading towards a crash. Instead, it is going through a correction phase that may last for several years.

- Despite slowing sales activity, home prices are still on the rise due to an inventory shortage, not a looming bubble burst.

- Stricter lending standards post the Great Recession have reduced the risk of a credit-driven collapse.

- The housing market is facing challenges of unaffordability and economic uncertainties impacting both buyers and sellers.

Currently, the housing market is at a standstill. High prices and increased mortgage rates are keeping buyers at bay, while sellers are hesitant to list their properties in fear of not finding a buyer. This has led to a slow market with more frequent price reductions, causing concern among consumers about the drastic shift from a hot market to a cold one.

Despite the apprehensions, most economists believe that the current state of the economy indicates a long-term correction rather than a crisis. The housing market today differs significantly from the conditions that led to the Great Recession nearly two decades ago when a housing bubble and risky lending practices triggered a collapse.

So, if you are a buyer or seller waiting on the sidelines with concerns about a potential housing market crash, this article delves into what a crash entails, why economists are optimistic, and the reasons behind the unease among buyers and sellers.

Insights from Redfin’s Chief Economist

“We are amidst a prolonged housing market correction, not a crash. Following the surge in prices and historic low inventory during the pandemic frenzy, the market needed a reset. What we are witnessing now is a gradual adjustment: slower sales, stabilized prices in many metropolitan areas, and buyers gaining leverage.” – Daryl Fairweather, Redfin Chief Economist

>> Read: Redfin’s 2026 Predictions: Welcome to The Great Housing Reset

Understanding a Housing Market Crash

A housing market crash refers to a sudden, significant, nationwide decline in home values. Crashes usually stem from broader economic or financial shocks like recessions, speculative lending surges, high inflation, or rising unemployment, which can swiftly impact the housing sector leading to oversupply or a sharp drop in demand.

During a crash, several common occurrences include:

- Rapid decline in home prices across the country

- Decrease in buyer demand often due to job losses, high interest rates, or delinquencies

- Sharp slowdown in home sales

- Increase in foreclosures and mortgage defaults as homeowners struggle with payments

Housing market crashes are usually linked to broader economic shifts like recessions, financial crises, or risky lending practices. The last significant real estate crash in the U.S. occurred during the Great Recession of 2008–2009, triggered by a burst housing bubble and mortgage lending crisis.

Reasons Why a Housing Market Crash Is Unlikely

Despite the current sluggish and pricey housing market accompanied by global economic uncertainties, experts are confident that a housing market crash is not on the horizon. Instead, it is experiencing an extended “reset” from the pandemic period when house prices and inflation soared.

“The notion of an impending crash arises whenever the economy undergoes significant changes,” stated Chen Zhao, Redfin Head of Economics Research. “However, current indicators point towards a relatively stable reset: Prices are stabilizing, mortgage rates are consistent, construction is increasing, and affordability is improving. Nonetheless, the market remains challenging, leading to concerns among individuals.”

Let’s delve deeper into why economists believe a housing crash is unlikely.

Gradual Rise in Home Prices and Expected Stabilization

In a pre-crash scenario, home prices might experience a sudden spike followed by a sharp decline as a housing bubble bursts. However, the current scenario differs as although prices are still increasing in many markets, the rate of growth has slowed down to around 1%, with most analysts projecting prices to plateau in 2026 and beyond as the market continues to adjust.

While there are exceptions regionally, parts of the Midwest and Northeast with affordable housing and limited inventory are witnessing price growth. Conversely, markets in the Sun Belt, notably Austin, have transitioned from being the hottest to the coldest markets in the nation with declining prices.

Stabilization of Mortgage Rates

A sudden fluctuation in mortgage rates can trigger significant shifts in the housing market, such as a surge in demand or a sharp decline in listings. However, the chances of this occurrence today, barring drastic measures from the Trump Administration, are minimal. While rates remain higher than the lows seen during the pandemic, they have stabilized compared to the rapid spikes in 2022 and 2023.

“The repercussions of a drastic rate decrease are uncertain, but it is unlikely to lead to a price surge,” Zhao continued. “One reason is that a rate drop might indicate an economic recession, limiting buyers’ purchasing power. Additionally, more properties may enter the market as sellers are released from their pandemic-era rates. This trend is already emerging: The number of homeowners with mortgage rates above 6% now exceeds those with rates below 3%, gradually increasing inventory.”

Resilient Labor Market

Unemployment and job growth significantly impact the housing market. Mass layoffs and rising unemployment are major triggers of housing crashes as they can lead to missed mortgage payments, forced sales, and increased foreclosures. A sudden decline in housing demand often follows a rapid loss of income due to layoffs, leading to increased supply as financially strained homeowners are compelled to sell.

The current scenario, however, paints a different picture.

“The job market has remained relatively stable, which is why we have not observed a surge in foreclosures or delinquencies,” Zhao added. “There are concerns regarding potential shifts in employment trends—particularly concerning the rise of artificial intelligence (AI) and the concentration of job growth almost solely in healthcare. Nonetheless, stable employment is a key reason economists do not foresee a wave of foreclosures or distressed sales.”

Stringent Lending Requirements

Regulations enforced after the 2008 financial crisis tightened mortgage lending standards to diminish risky loans and prevent another widespread mortgage credit collapse. These regulations, such as requiring banks to hold more reserves to cover potential lending losses, lessen the likelihood of another credit-induced economic collapse.

“The stringent lending standards implemented in 2010 and reinforced in 2024 make it improbable for another credit-driven economic collapse to occur,” noted Fairweather. “Enhanced oversight and transparent underwriting have rendered the housing market significantly more resilient than it was twenty years ago.”

Concerns of Buyers and Sellers Regarding a Housing Market Crash

Although a real estate crash seems unlikely, everyday Americans are grappling with the repercussions of a volatile and highly unaffordable housing market—particularly impacting younger generations.

To gain a better comprehension of the challenges, let’s analyze some key data concerning the current market.

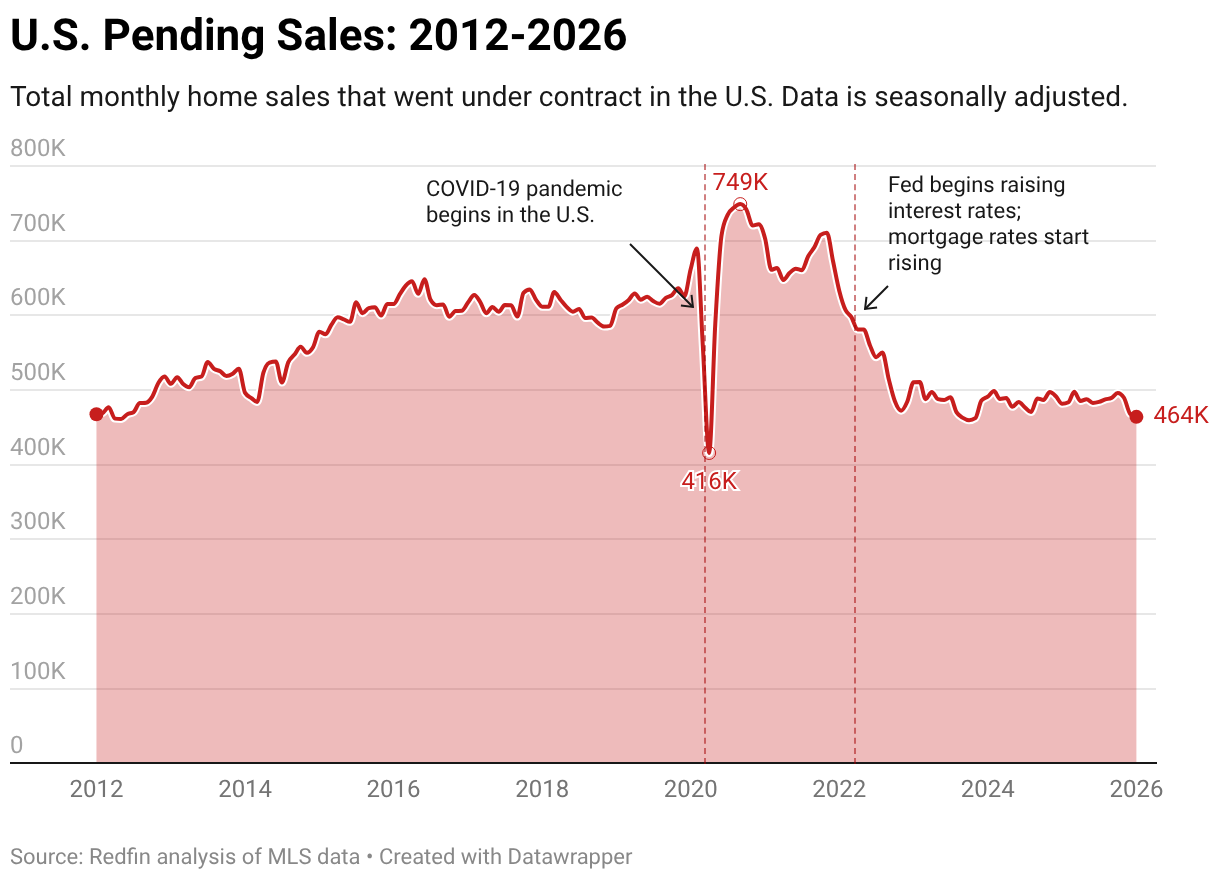

The Rollercoaster Ride of the Pandemic Housing Market

The pandemic wreaked havoc on the housing market, causing significant fluctuations that instilled fear of a potential crash among experts.

Real estate activity came to a halt in early 2020 before skyrocketing to unprecedented levels in 2021-2022 as remote work and historically low mortgage rates fueled a buying frenzy, primarily in the Sun Belt region. However, when mortgage rates surged and affordability plummeted in 2022–2023 due to unprecedented inflation, demand sharply declined.

Currently, the housing market has decelerated significantly, with buyers priced out and sellers awaiting a resurgence in activity. Price reductions are common nationwide and particularly prevalent in the Sun Belt region, where most people relocated during the pandemic—especially in Austin, Nashville, and San Antonio.

There are still a few outlier cities in the Midwest and Northeast witnessing brisk sales and price hikes, such as Buffalo and Milwaukee, primarily due to their affordability and limited housing options.

A Possible “Housing Bubble”

Home prices have continuously set new monthly records for over two years, sparking concerns of a potential “bubble” situation where prices are artificially inflated. Despite the slowdown in price growth from the rapid pace during the pandemic, prices are still increasing and remain near record highs in numerous regions, primarily attributed to a significant inventory shortage which is gradually improving.

However, some experts argue that the primary issue lies in the scarcity of affordable homes. Those currently able to afford homes are generally making purchases, while a vast majority of consumers are priced out of the market.

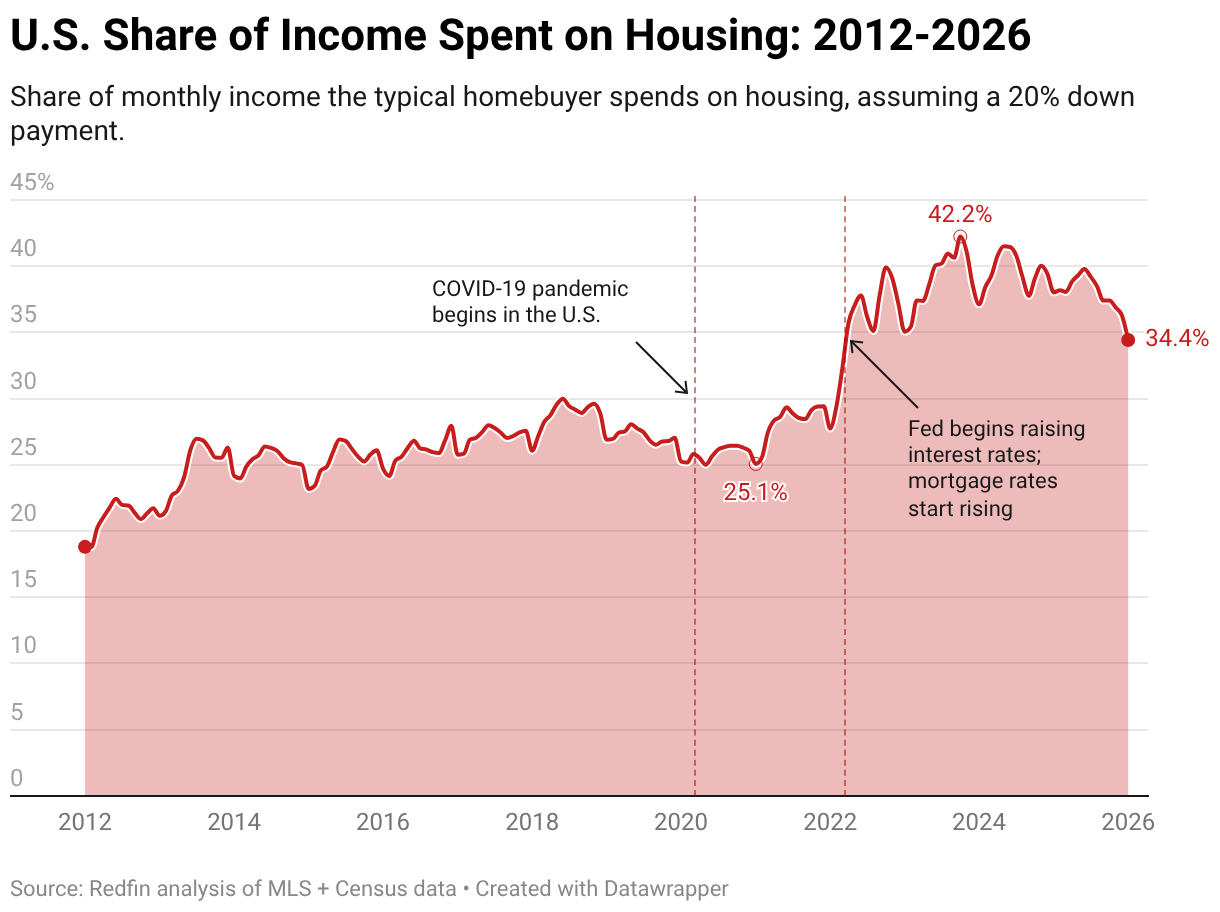

Record-Low Affordability and Economic Concerns

A prolonged period of uncertainty and historically low affordability has left Americans grappling with elevated mortgage rates, persistently high home prices, and broad economic anxieties, making homeownership a distant dream for many.

As per Redfin data, the average homebuyer is allocating around 34% of their income towards housing (as of January 2026), while home prices have surged approximately 40% since the pandemic.

Nevertheless, with the slowdown in price growth and wage hikes, affordability is gradually improving. There is a possibility that by 2030, prices will